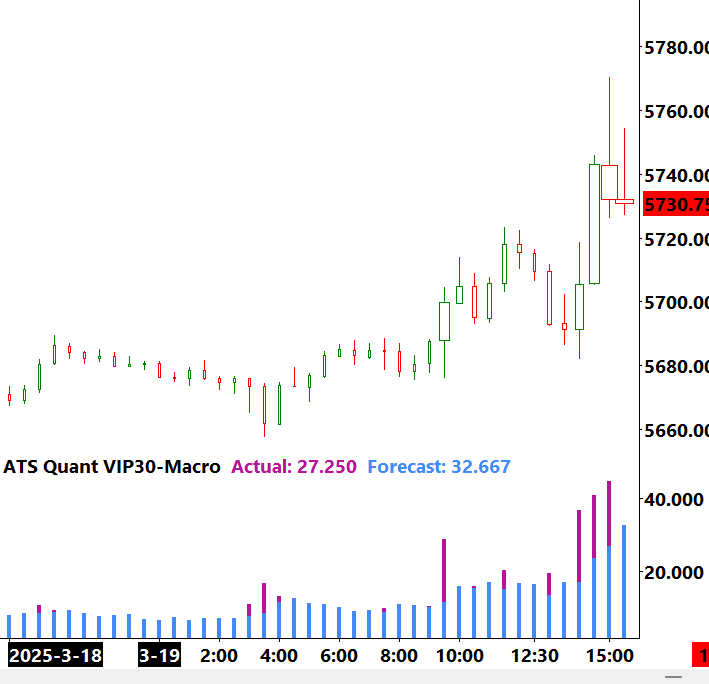

ATS Quant Volatility Intraday Position 30 Macro

This machine learning system forecasts volatility for the next bar.

The system can be applied to the following instruments:

-E-Mini S&P 500 Futures

-E-Mini Nasdaq 100 Futures

-Gold Futures

-WTI Crude Oil (CL) Futures

-Australian Dollar Futures

-British Pound Futures

-Canadian Dollar Futures

-Euro FX Futures

-Japanese Yen Futures

*additional macro instruments not listed will be included in future updates

*E-Mini S&P 500 pictured

The model was trained to read the orderflow and forecast future volatility. This means that the model dynamically adjusts its forecast based on shifts in market states.

The system understands the difference between the microstructure of each instrument and thus adjusts its forecasts based on the current instrument.

Volatility forecasting can improve trade location, risk management, trade management, limit false breakouts, etc.

This model is designed specifically for 30 min samples (i.e. candles, numbers bars, etc).

Updates and improved versions of this model are included with this subscription.

This version of the model integrates directly into Sierra Charts.

At sign-up you will need a valid Sierra Charts account. This model is valid across all Sierra Charts package options.

This machine learning system forecasts volatility for the next bar.

The system can be applied to the following instruments:

-E-Mini S&P 500 Futures

-E-Mini Nasdaq 100 Futures

-Gold Futures

-WTI Crude Oil (CL) Futures

-Australian Dollar Futures

-British Pound Futures

-Canadian Dollar Futures

-Euro FX Futures

-Japanese Yen Futures

*additional macro instruments not listed will be included in future updates

*E-Mini S&P 500 pictured

The model was trained to read the orderflow and forecast future volatility. This means that the model dynamically adjusts its forecast based on shifts in market states.

The system understands the difference between the microstructure of each instrument and thus adjusts its forecasts based on the current instrument.

Volatility forecasting can improve trade location, risk management, trade management, limit false breakouts, etc.

This model is designed specifically for 30 min samples (i.e. candles, numbers bars, etc).

Updates and improved versions of this model are included with this subscription.

This version of the model integrates directly into Sierra Charts.

At sign-up you will need a valid Sierra Charts account. This model is valid across all Sierra Charts package options.